Internal Audit

Audit & Beyond | Oct. 21-23, 2025 | Early bird: Save $400

May 10, 2022 • 7 min read

Brett Luis & Joe Kim

Process-level automation — also known as hyperautomation — involves the orchestrated use of multiple technologies to automate as many business and IT processes as possible. According to predictions from Gartner, McKinsey, and Deloitte, hyperautomation is one of the top technology trends of 2022.

In our Internal Audit Hyperautomation Blueprint Series, we explore examples of business processes typically selected for SOX and internal audit testing that contain many opportunities for hyperautomation. Download your free copy of our first whitepaper in this series — which explores opportunities in the purchasing and payable lifecycle — and read on below for an overview of how to incorporate RPA, Advanced Analytics, Data Visualizations, and API/IPaaS in purchasing and payables, including:

Purchasing and payables is a frequently audited business process, one that auditors have long sought to create efficiencies in. With the exception of the payroll process, the accounts payable process accounts for the largest proportion of spend at most organizations. Accounts payable performance has a direct bearing on:

Further, it can be fraught with complexity due to the high volume of transactions, multiple integrated systems, banks, and payment types — leading to an increase in opportunity and incentive for fraud. The following are three groups of automation areas in the purchasing and payables lifecycle: Discovery Analytics/Data Profiling, ICFR Procedures, and Fraud Techniques. For each of these groups, we’ve included an excerpt from a larger list of example procedures — found when you download the full eBook — that can be used to implement automation in that category.

The following is an overview of the systems and data files used across the accounts payable lifecycles.

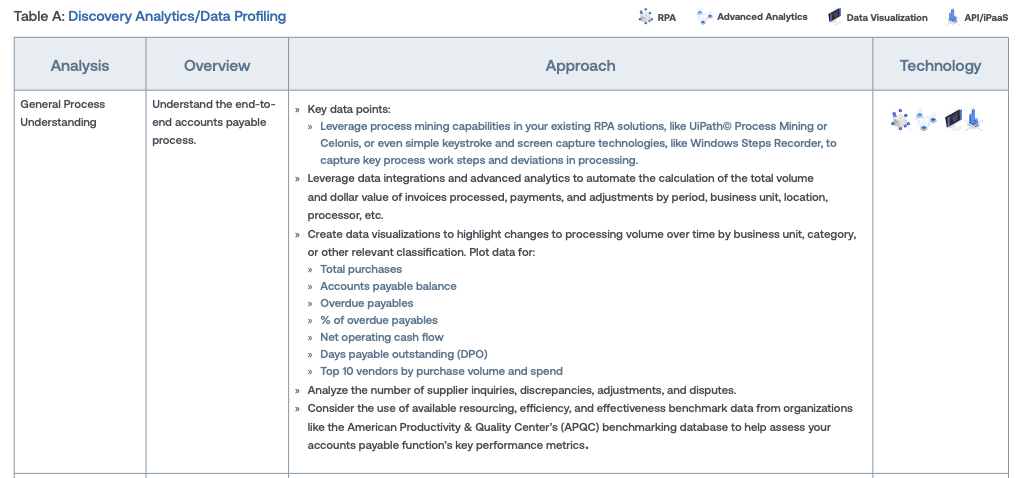

Leveraging your accounts payable function’s existing dashboards, analytics, or technologies — like process mining — can provide valuable insights into transaction processing volumes, trends, error rates, and opportunities for efficiency. If your accounts payable function has not conducted transformational initiatives like spend analysis and automation, you will likely identify significant value-add observations by conducting your own discovery analysis. The following is an example procedure you can use to help understand the business process, uncover insights, and substantiate the objectives and focus of your audit.

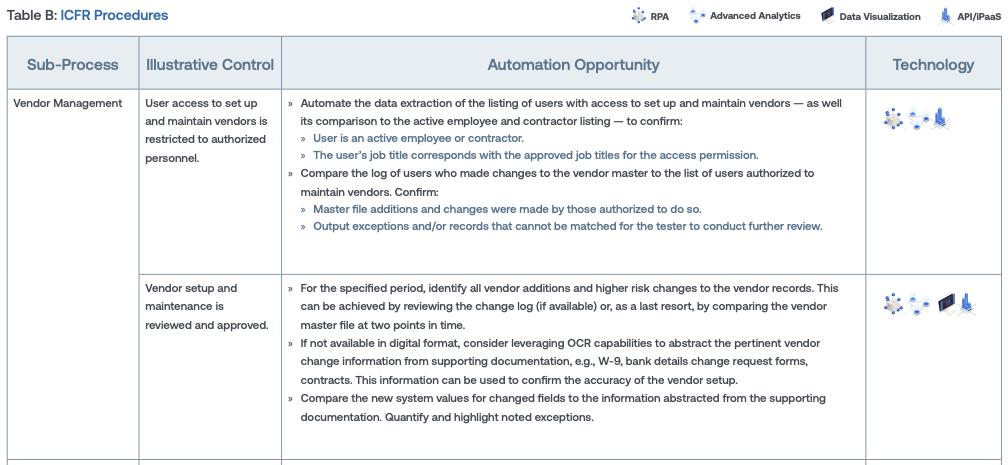

Traditional accounts payable cycle internal control testing procedures offer an array of opportunities to leverage technology to improve coverage, accuracy, and efficiency. By pursuing continuous auditing through automating evidence collection and suitable testing procedures, audit teams are empowered to focus their resources on higher-value tasks, reducing audit fatigue and ultimately transforming their processes by eliminating non-value-add manual tasks. The following is an example of using automation in your ICFR coverage.

According to the 2020 ACFE Report to the Nations, accounts payable billing schemes are the most common form of asset misappropriation and cause a high median loss, making this type of fraud a particularly significant risk. The average median loss from a billing scheme is $100,000 and these schemes persist for 24 months on average before detection. As audit teams embrace transformational technologies to help increase the effectiveness and coverage of their audit and fraud procedures, we will likely see a reduction in detection times and an increase in the internal audit detection percentage rate.

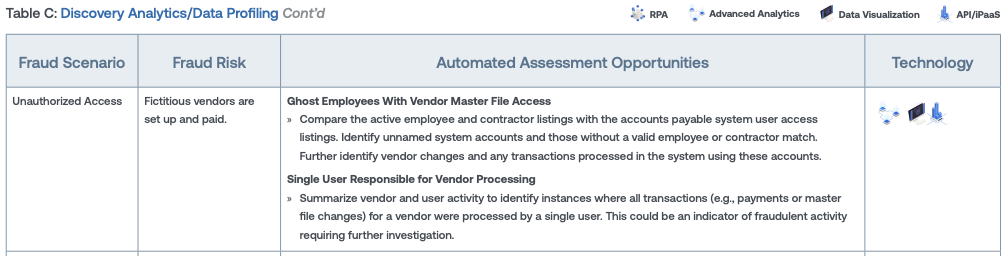

The following is an example of how internal audit teams may leverage hyperautomation technologies to help detect accounts payable fraud schemes.

For a deeper dive into the most impactful automation opportunities across the purchasing and payables lifecycle, download the full guide: Internal Audit Hyperautomation Blueprint: Purchasing and Payables. Stay tuned for further installments of our Internal Audit and Hyperautomation Blueprint Series that will explore opportunities across other SOX and audit business processes.

Brett Luis was a VP of Product at AuditBoard, where he focused on enhancing audit products through analytics, automation, and other advanced technologies. Before joining AuditBoard, Brett was on the front lines — supporting public companies in standing up robust internal audit and SOX compliance programs — and in the audit trenches, leading attestation reporting engagements and the IT component of the internal controls and financial statement audits for public registrants. Connect with Brett on LinkedIn.

Joe Kim is a is a Director of Product at AuditBoard, serving as the product leader for AuditBoard’s audit software product line and leading innovation in this space by empowering the next generation of auditors using transformative technology. Joe brings 16 years of experience in both public and private accounting with specializations in workforce automation and data analytics. Connect with Joe on LinkedIn.